Methodological clarification of using cash register receipts from 2024 in 2025 and their application in 2025 from the perspective of VAT law

Based on methodological guidelines, the creation of cash register receipts in 2025 that used deposit payments and single-purpose vouchers from 2024 is being clarified. The methodological guidelines also concern cancellation documents - return of goods sold with a discount from 2024.

When applying the relevant tax rate, the decisive fact is the day of tax obligation origin

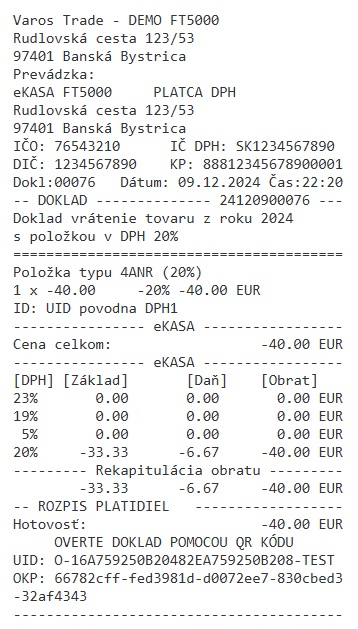

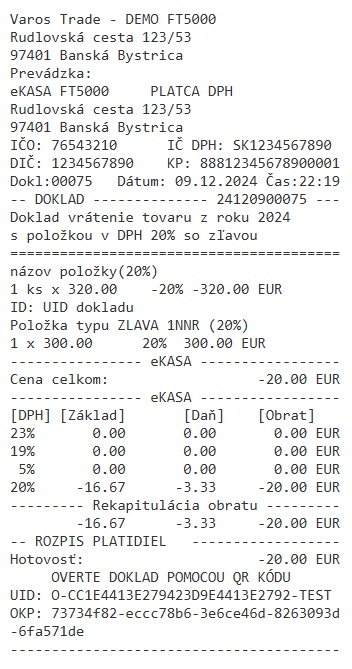

Return of goods - document cancellation from 2024 in 2025

When canceling a document from 2024, document items must be canceled at the same VAT rates at which the sale of these items was made. If a discount was used on the original document, a positive item must be used to return the discount at the same VAT rate at which the discount was provided in 2024.

Example of document cancellation with discount from 2024:

SONY TV 1x 1500 VAT 20% -1500.00 EUR

Discount provided 2024 1x 150 VAT 20% 150.00 EUR

_____________________________________________________________________

Total price -1350.00 EUR

_____________________________________________________________________

[VAT] [Base] [Tax] [Turnover]

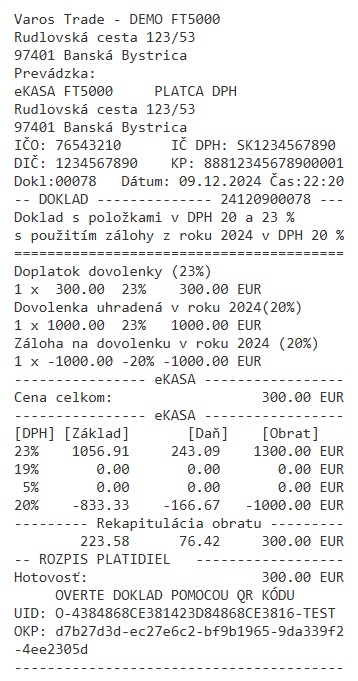

20% -1125.00 -225.00 -1350.00 EURApplication of deposit received from 2024 in 2025

If the taxpayer received a deposit by 31.12.2024 for goods or services that will be delivered after 31.12.2024, the tax rate valid at the time of each tax obligation origin must be applied.

This means:

-

Tax rate valid at the time of deposit receipt. If the deposit was received in 2024 for part of the goods paid by this deposit payment, the tax rate of 20% or 10% applies depending on which VAT rate the deposit was received.

-

Tax rate valid at the time of goods or services delivery. If goods or services were delivered in 2025, the tax rate of 23%, 19%, or 5% applies to the remaining part of the price after deducting the deposit received from 2024.

Example of document with deposit application from 2024:

Bali vacation 0.2 x 2500 VAT 20% 500.00 EUR

Deposit from 2024 1x 500 VAT 20% -500.00 EUR

Bali vacation 2025 0.8x 2000 VAT 23% 2000.00 EUR

_____________________________________________________________________

Total price 2000.00 EUR

_____________________________________________________________________

[VAT] [Base] [Tax] [Turnover]

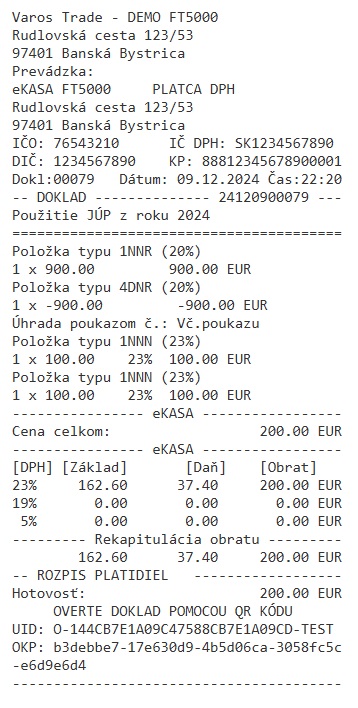

23% 1626.02 373.98 2000.00 EURApplication of single-purpose voucher SPV from 2024 in 2025

If an SPV purchased in 2024 is used in 2025, the document must contain goods or services with the same VAT rate. The tax rate valid at the time of SPV purchase must be applied.

This means:

-

Tax rate valid at the time of SPV purchase. If the SPV was purchased in 2024 for part of the goods paid by SPV, the tax rate of 20% or 10% applies depending on which VAT rate the SPV was sold.

-

Tax rate valid at the time of goods or services delivery. If goods or services were delivered in 2025, the tax rate of 23%, 19%, or 5% applies to the remaining part of the price after deducting the deposit received from 2024.

Example of document with SPV application from 2024:

Tatras vacation 0.5 x 1000 VAT 20% 500.00 EUR

SPV from 2024 1x 500 VAT 20% -500.00 EUR

Tatras vacation 2025 0.8x 2000 VAT 23% 2000.00 EUR

_____________________________________________________________________

Total price 2000.00 EUR

_____________________________________________________________________

[VAT] [Base] [Tax] [Turnover]

23% 1626.02 373.98 2000.00 EURTotal price of cash register receipt from the perspective of VAT input application

As of 01.01.2025, the Value Added Tax Law 222/2004 Z.z. was also modified.

The amendment to § 74 section 3, letter b) also concerns the issuance of documents for VAT input deduction purposes. The limit of the total price of a cash register receipt that can be considered a “simplified invoice” for VAT deduction from a legal perspective has been reduced to 400€

The possibility of using a cash register receipt or cash payment of an invoice from eKasa for VAT input deduction for amounts exceeding 400€ is only when these documents contain all invoice requirements.

Creation of cash register receipts in 2025 for documents issued in 2024

| No. | Type of cash register receipt | INPUT FILE | PRINT OUTPUT |

|---|---|---|---|

| 1 | Receipt with items in VAT 20 and 23% using 2024 voucher in VAT 20% | Show | Show |

| 2 | Receipt with items in VAT 20 and 23% using 2024 deposit in VAT 20% | Show | Show |

| 3 | Receipt with items in VAT 10 and 23% using 2024 voucher in VAT 10% | Show | Show |

| 4 | Receipt for return of goods from 2024 with item in VAT 20% | Show | Show |

| 5 | Receipt for return of goods from 2024 with discount in VAT 20% | Show | Show |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Number of tax levels in 2025 that eKasa must support

Regarding support for 10% and 20% rates after 1.1.2025 in ORP. eKasa must allow the use of 20% and 10% VAT rates for deducted deposits, use of single-purpose vouchers, and also for goods returns/corrections, and it cannot be replaced by credit notes or other similar methods.

This means support for rates 0%, 5%, 10%, 19%, 20%, 23% after 1.1.2025.

eKasa without declared support for all mentioned rates in 2025 does not meet legislative requirements and the Certification Authority will not approve such a solution.

For this reason, the control sequence table has been expanded with new control sequences.

New JSON sequences to support the third tax level

VAT Rate - VatRate

VatRate – variable to determine VAT rate for document item.

Integer [1-7]{1}

| VatRate | Description |

|---|---|

| 1 | VAT1 - Standard VAT rate 23% |

| 2 | VAT2 - Reduced VAT rate 19% |

| 3 | VATFREE - VAT exempt |

| 4 | VAT3 - Reduced VAT rate 5% |

| 5 | VAT1OLD - Original standard VAT rate 20% |

| 6 | VAT2OLD - Original reduced VAT rate 10% |

| 7 | VAT3OLD - Original reduced VAT rate x% |